“Bukan Fund, Bukan Trust”: Saylor Menarik Garis saat MSCI Mempertimbangkan Nasib MicroStrategy

CEO MicroStrategy Michael Saylor menanggapi ulasan klasifikasi dari MSCI dengan menggambarkan perusahaannya sebagai bisnis operasi hybrid, bukan sebuah dana investasi.

Klarifikasi ini muncul di tengah konsultasi formal tentang bagaimana perusahaan treasury aset digital (DATs) harus diperlakukan dalam indeks ekuitas utama, sebuah keputusan yang bisa memiliki dampak besar pada MSTR.

Michael Saylor Tegaskan: “MicroStrategy Bukan Fund atau Trust” di Tengah Pengawasan MSCI

Dalam sebuah postingan detail di X (Twitter), Saylor menekankan MicroStrategy bukanlah sebuah dana, bukan trust, dan bukan perusahaan holding.

“Kami adalah perusahaan operasi yang diperdagangkan secara publik dengan bisnis perangkat lunak senilai US$500 juta dan strategi treasury unik yang menggunakan Bitcoin sebagai modal produktif,” ujar dia menjelaskan.

Pernyataan ini memposisikan MicroStrategy lebih dari sekadar holder Bitcoin, dengan Saylor mencatat bahwa dana dan trust memegang aset secara pasif.

“Perusahaan holding hanya duduk di atas investasi. Kami menciptakan, menyusun, mengeluarkan, dan mengoperasikan,” tambah Saylor, menyoroti peranan aktif perusahaan dalam keuangan digital.

Tahun ini, MicroStrategy menyelesaikan lima penawaran publik sekuritas kredit digital: STRK, STRF, STRD, STRC, dan STRE. Jumlah ini mencapai lebih dari US$7,7 miliar dalam nilai nominal.

Perlu dicatat, Stretch (STRC) adalah instrumen treasury yang didukung oleh Bitcoin dan menawarkan hasil USD variabel bulanan kepada investor institusional dan ritel.

Saylor menggambarkan MicroStrategy sebagai perusahaan keuangan terstruktur yang didukung oleh Bitcoin yang beroperasi di pertemuan pasar modal dan inovasi perangkat lunak.

“Tidak ada kendaraan pasif atau perusahaan holding yang bisa melakukan apa yang kami lakukan,” ucap dia, menekankan bahwa klasifikasi indeks tidak mendefinisikan perusahaan tersebut.

Mengapa Keputusan MSCI Penting

Konsultasi MSCI dapat mengklasifikasikan kembali perusahaan seperti MicroStrategy sebagai dana investasi, menjadikannya tidak memenuhi syarat untuk indeks utama seperti MSCI USA dan MSCI World.

Pengecualian ini bisa memicu miliaran dalam arus keluar pasif dan meningkatkan volatilitas pada $MSTR, yang saat ini turun sekitar 70% dari titik tertingginya.

Taruhannya melampaui MicroStrategy. Pembelaan Saylor menentang norma tradisional keuangan (TradFi), mempertanyakan apakah perusahaan operasi yang didorong oleh Bitcoin dapat mempertahankan akses ke modal pasif tanpa dilabeli sebagai dana.

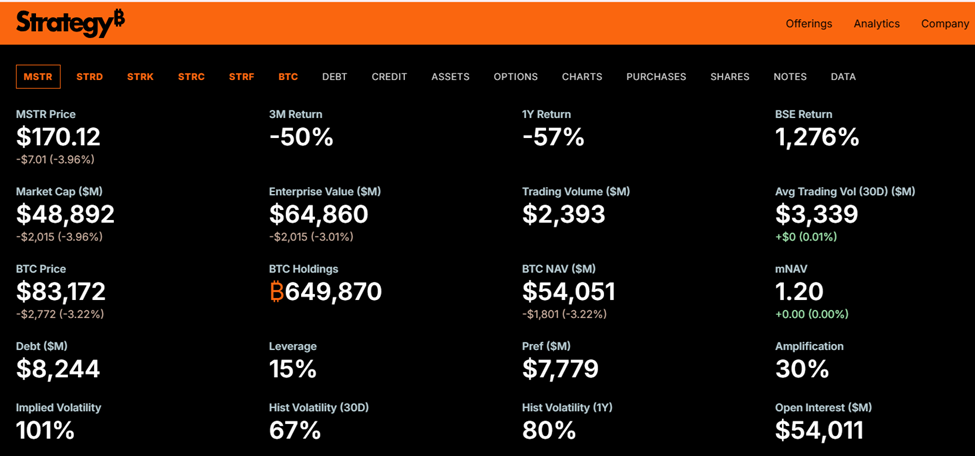

MicroStrategy memegang 649.870 Bitcoin, dengan biaya rata-rata US$74.430 per koin. Nilai perusahaannya mencapai US$66 miliar, dan perusahaan ini mengandalkan penawaran ekuitas dan utang terstruktur untuk mendanai strategi akumulasi Bitcoinnya.

Putusan MSCI, yang diharapkan keluar pada 15 Januari 2026, bisa menguji kelayakan model treasury hybrid seperti ini di pasar publik.